Reverse Mortgage as a Retirement Alternative Having alternative sources of retirement income is critical for those who are currently retired, those retiring in the near future, and those planning to retire in the next 30 to 40 years. One alternative available to many Americans is a reverse mortgage. Surveys show that Americans tend to store […]

Articles

HECM Reverse Mortgages: Now or Last Resort?

This study outlines recent changes in the reverse mortgage market and attempts to shed light on two simple questions: Which client-specific and capital market factors should a practitioner emphasize; and Based on these critical factors, how does early or delayed establishment influence whether a reverse mortgage can improve the probability of clients’ maintaining their retirement […]

Standby Reverse Mortgages: A Risk Management Tool for Retirement Distributions

The importance of effective distribution strategies is rapidly increasing as 78 million baby boomers approach retirement over the next decade.1 The diminished role of defined benefit plans, longer life expectancy, escalating health care costs, and poor equity returns over the last decade are just a few of the issues confronting retirees that create a challenging […]

Increasing the Sustainable Withdrawal Rate Using the Standby Reverse Mortgage

Research published in the Journal of Financial Planning has estimated that retirees can expect to safely withdraw roughly 4 percent of their initial portfolio value, adjusted for inflation, each year in retirement (Bengen 1994). However, recent research has questioned whether the 4 percent rule is safe for retirees who are projected to face lower returns […]

Reversing the Conventional Wisdom: Using Home Equity to Supplement Retirement Income

The overriding objective for many retirees is to maintain cash flow throughout their retirement years, to avoid “running out of money” in their later years. Cash flow survival is the central theme of this article. This paper examines three strategies for using home equity, in the form of a reverse mortgage credit line, to […]

The Hidden Value of a Reverse Mortgage Standby Line of Credit

Several recent research articles published in the Journal of Financial Planning have investigated how opening a standby line of credit through a reverse mortgage and strategically spending from this line of credit can help improve the sustainability of retirement income strategies. In this article, I show that the benefits of opening a home-equity conversion mortgage […]

Incorporate Home Equity into Your Retirement Income Planning

Wade Pfau’s article Incorporating Home Equity into a Retirement Income Strategy describes six methods for incorporating home equity into a retirement income strategy through a reverse mortgage. Generally, strategies that spend the home equity more quickly increase the overall risk for the retirement plan. More upside potential is generated by delaying the need to take distributions from […]

Recovering a Lost Deduction

This article, originally published in the Journal of Taxation, examines the conditions, requirements, and limitations on deductions of the interest accrued on reverse mortgage loans. Although the conventional approach for passing a borrower’s home equity to heirs generally results in the loss of the deduction for reverse mortgageloan interest, the deduction may be used if it […]

Tax Deductions and Reverse Mortgages

You may have tax deductions you can use if you have a FHA-insured Home Equity Conversion Mortgage (HECM). Tom Davison’s in-depth article on reverse mortgage’s tax opportunities and obligations for annual tax reporting. Davison includes information on the following topics: Loan Proceeds are Not Taxable Income Interest Deduction Mortgage Insurance Premium (MIP) Deduction Interest on Acquisition […]

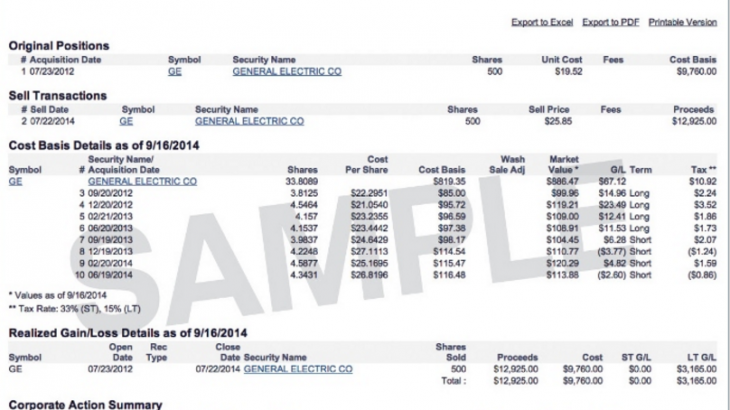

How to Calculate Your Capital Gains Tax

When it comes to calculating your capital gains tax, understanding your cost basis is crucial. Essentially, the cost basis of an investment is what you paid for it. Working out any capital gains when you sell an investment is just a matter of subtracting your cost basis from your sale price. It sounds simple enough, […]